Introduction

Significant changes are coming for retirement savers in 2026! If you’ve been contributing to your 401(k), the new 401(k) contribution limits for 2026 could mean you’ll have more room to grow your nest egg — and enjoy bigger tax advantages along the way. Let’s break down what’s changing, why it matters, and how you can make the most of these updates.

What Is a 401(k) Plan?

A 401(k) plan is a retirement savings account offered by many employers. It allows you to contribute a portion of your paycheck before taxes (in a traditional 401(k)) or after taxes (in a Roth 401(k)). Over time, your money grows through investments — typically in mutual funds, ETFs, or company stock.

Why 401(k) Contribution Limits Matter

Each year, the IRS sets a maximum limit on how much you can contribute to your 401(k). These limits are necessary because they determine:

- How much can you save tax-deferred or tax-free

- The amount of employer match you can receive

- Your total potential retirement savings growth

When the IRS increases these limits, it’s an excellent opportunity to save more efficiently.

Overview of 2026 Contribution Changes

4.1 Employee Contribution Limit Increase

In 2026, the employee contribution limit is expected to rise to around $24,500, up from $23,000 in 2025. This adjustment reflects inflation and the government’s push to help Americans prepare for retirement more effectively.

4.2 Catch-Up Contributions for Older Workers

If you’re 50 or older, you can make catch-up contributions — an extra amount added beyond the standard limit. For 2026, these amounts may increase to $8,000 (up from $7,500 in 2025), providing seasoned workers with an opportunity to accelerate their savings before retirement.

4.3 Employer Match Adjustments

Employers can contribute up to a combined total (employee + employer) of $68,000 or $75,000 for those 50 and older. This means that if your company offers matching contributions, you could potentially grow your account much faster.

How the 2026 Limit Compares to 2025

Here’s a quick snapshot of the expected differences:

| Year | Employee Limit | Catch-Up (50+) | Combined Limit |

| 2025 | $23,000 | $7,500 | $69,000 |

| 2026 | $24,500 | $8,000 | $75,000 |

Even small increases make a big difference over time — especially with compound growth working in your favor.

Factors Influencing the 2026 Increase

6.1 Inflation Adjustments

Rising costs of living play a significant role in these updates. As inflation affects the dollar’s purchasing power, the IRS adjusts contribution limits to help savers maintain their retirement goals.

6.2 Economic Growth and Policy Shifts

Government policies and labor market trends also influence these numbers. The SECURE Act 2.0, for instance, already paved the way for automatic enrollment and expanded contribution flexibility.

New IRS Rules for 2026

7.1 Pre-Tax vs. Roth Contributions

The IRS continues to emphasize flexibility. Employees can choose between pre-tax contributions (traditional 401(k)) for immediate tax relief or after-tax contributions (Roth 401(k)) for tax-free withdrawals later.

7.2 Catch-Up Contribution Rule Changes

Starting in 2026, high earners (making over $145,000) may be required to make catch-up contributions in a Roth 401(k) — meaning they’ll pay taxes now but enjoy tax-free growth later.

7.3 Employer Reporting Requirements

Employers will face stricter reporting standards to ensure compliance with updated IRS rules, especially regarding Roth designations and matching contributions.

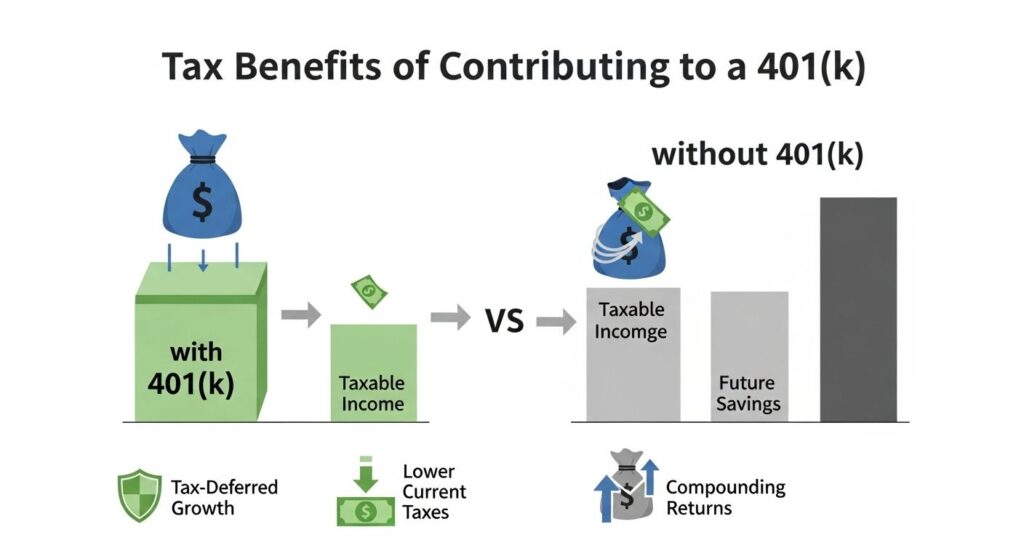

Tax Benefits of Contributing to a 401(k)

8.1 Traditional 401(k) Tax Advantages

- Contributions reduce your taxable income

- Taxes are deferred until withdrawal

- Ideal for people expecting a lower income in retirement

8.2 Roth 401(k) Tax Advantages

- Contributions are made with after-tax income

- Withdrawals in retirement are tax-free

- Perfect for younger savers expecting higher future earnings

8.3 Compound Growth and Long-Term Gains

Think of compounding like a snowball rolling down a hill — your earnings generate even more earnings. The earlier you start, the bigger the snowball gets.

How to Maximize Your 401(k) Contributions

9.1 Automate Your Savings

Set up automatic contributions so saving for retirement becomes effortless — like paying yourself first every month.

9.2 Take Full Advantage of Employer Matches

If your employer offers a 401(k) match, don’t leave free money on the table! Contribute at least enough to capture the whole game.

9.3 Balance Contributions Between Accounts

Consider diversifying between 401(k) and IRA accounts for better tax and investment flexibility.

Impact on High-Income Earners

Higher limits mean greater tax advantages. However, Roth catch-up rules and income caps may affect high earners’ strategies. Consulting a financial advisor could help optimize your mix of traditional and Roth savings.

Impact on Small Business Owners

If you own a business, the increased employer contribution limits could help you attract and retain talent while reducing taxable income through business deductions.

Common Mistakes to Avoid with 401(k) Contributions

- Ignoring employer match opportunities

- Failing to adjust contributions annually

- Withdrawing early and triggering penalties

- Not rebalancing your investment portfolio

Avoiding these pitfalls ensures your savings stay on track.

Future Outlook Beyond 2026

Experts predict continued adjustments as inflation persists and retirement needs evolve. Legislative updates, such as the SECURE Act 3.0, may further enhance contribution flexibility and access to retirement savings.

Practical Steps to Prepare for the New Limits

- Review your current contributions.

- Plan to increase them gradually before 2026.

- Consult a tax professional about Roth options.

- Take advantage of employer matches.

- Stay informed on IRS announcements.

Conclusion

The new 401(k) contribution limits for 2026 offer exciting opportunities for retirement savers. With higher limits, new rules, and enhanced tax benefits, now’s the perfect time to revisit your savings strategy. By staying proactive and informed, you can maximize every dollar you contribute and build a stronger financial future.

FAQs

1. What is the 401(k) contribution limit for 2026?

The limit is expected to increase to $24,500 for employees, with an additional $8,000 in catch-up contributions available for those aged 50 and above.

2. Will the Roth 401(k) rules change in 2026?

Yes, high earners may be required to make catch-up contributions in a Roth 401(k).

3. Can employers contribute more in 2026?

Yes, the total combined limit (employee plus employer) will increase to approximately $75,000.

4. Are 401(k) contributions tax-deductible?

Traditional 401(k) contributions reduce your taxable income, while Roth 401(k) contributions grow tax-free.

5. How can I prepare for the 2026 changes?

Increase your contributions gradually, review your plan options, and consult a financial planner for personalized advice.